The African Development Bank's African Economic Outlook 2026 (the "Report")

arrives at a pivotal moment for African economies. Published against a backdrop

of geopolitical fragmentation, tightening global financial conditions and declining

external development assistance. Its central proposition is clear: Africa's long-term

development trajectory will depend less on external finance and more on its ability

to mobilise, structure and deploy its own capital at scale.

This commentary examines the legal dimensions of that challenge and the

opportunities it presents for investors, governments, development finance

institutions and market participants.

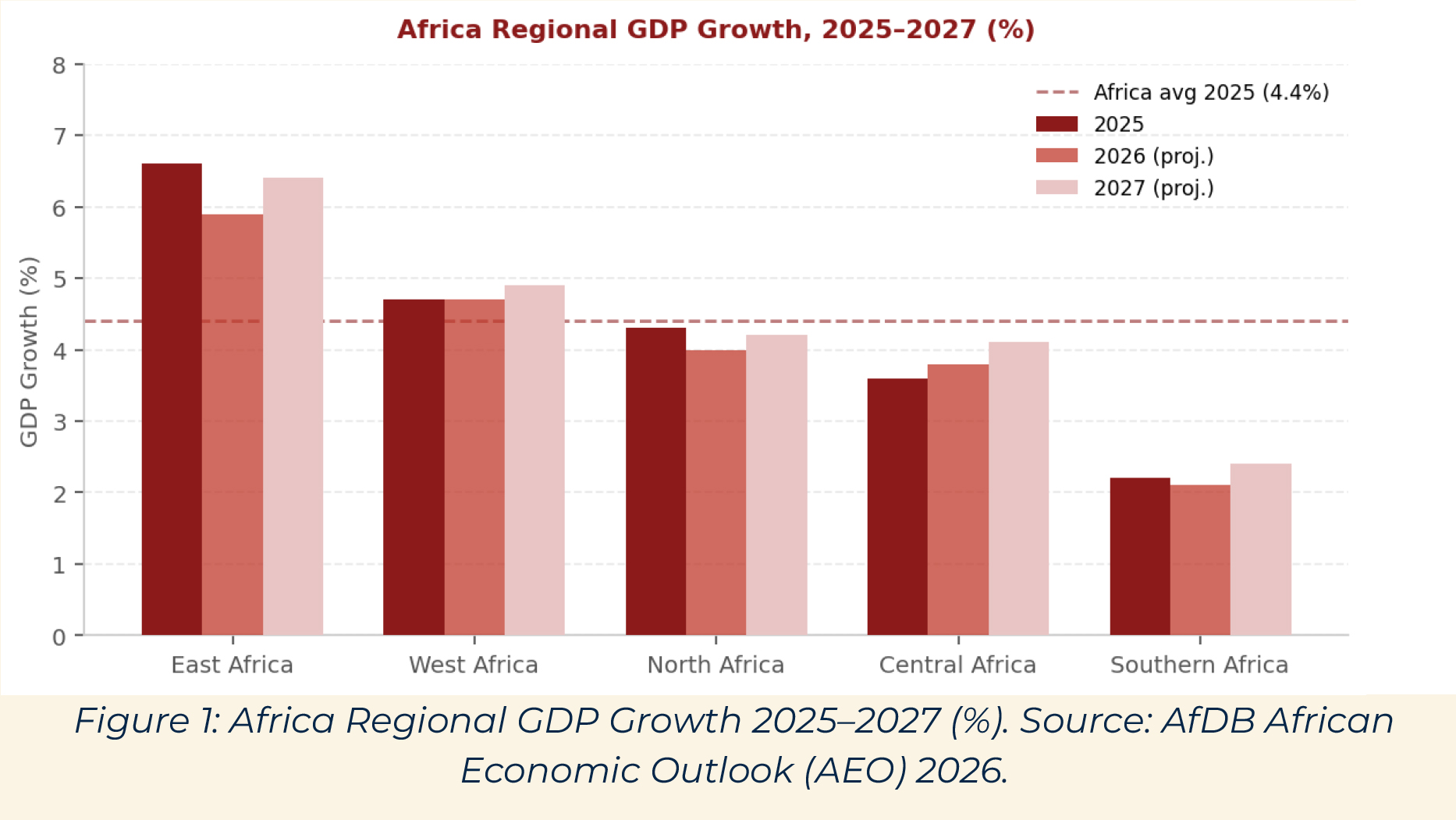

Africa’s headline growth is striking: average GDP growth of 4.4 percent in 2025,

with 22 economies above 5 percent, projected to sustain 4.2 percent in 2026 before

strengthening to 4.4 percent in 2027. Improved macroeconomic management,

stronger agricultural output, elevated commodity prices and ongoing structural

reforms have maintained Africa’s position among the world’s fastest-growing

regions despite significant external headwinds.

The regional picture is more nuanced. East Africa leads at 6.6 percent (2025),

moderating to 5.9 percent (2026) as Middle East-linked energy costs weigh on

activity, before rebounding to 6.4 percent (2027). West Africa holds at

approximately 4.7 percent, supported by agriculture and infrastructure

investment. North Africa eases to 4.0 percent amid weaker tourism and supply

chain disruptions. Central Africa edges up to 3.8 percent on sustained oil prices,

while Southern Africa remains muted at 2.1 percent, constrained by weaker mining

output and elevated energy costs.

But the risks are real. Inflation at 10.4 percent in 2026. Double-digit inflation across

several jurisdictions. Geopolitical tensions, exchange rate depreciation and global

fragmentation amplifying debt and fiscal vulnerabilities. For legal advisers, these

realities hit transaction structuring head-on: currency risk allocation, sovereign

support arrangements, force majeure protections, debt refinancing frameworks

and political risk mitigation all assume heightened importance.

The global financing environment has changed, structurally and perhaps

permanently. Official development assistance, Chinese bilateral lending and

access to international capital markets have all declined materially, with little

indication of reversal. External finance is no longer just tighter. It is unreliable.

The response must be a decisive shift towards African financial agency: stronger

domestic resource mobilisation, deeper capital markets, integrated financial

systems, expanded private sector participation. This is not merely an economic

objective, it is a legal and institutional one.

Pension funds, sovereign wealth funds, insurance companies and domestic asset

managers cannot deploy capital at scale without legal certainty, clear investment

mandates and appropriately structured products. The challenge goes beyond

capital formation, it is about the architecture through which savings become

productive investment.

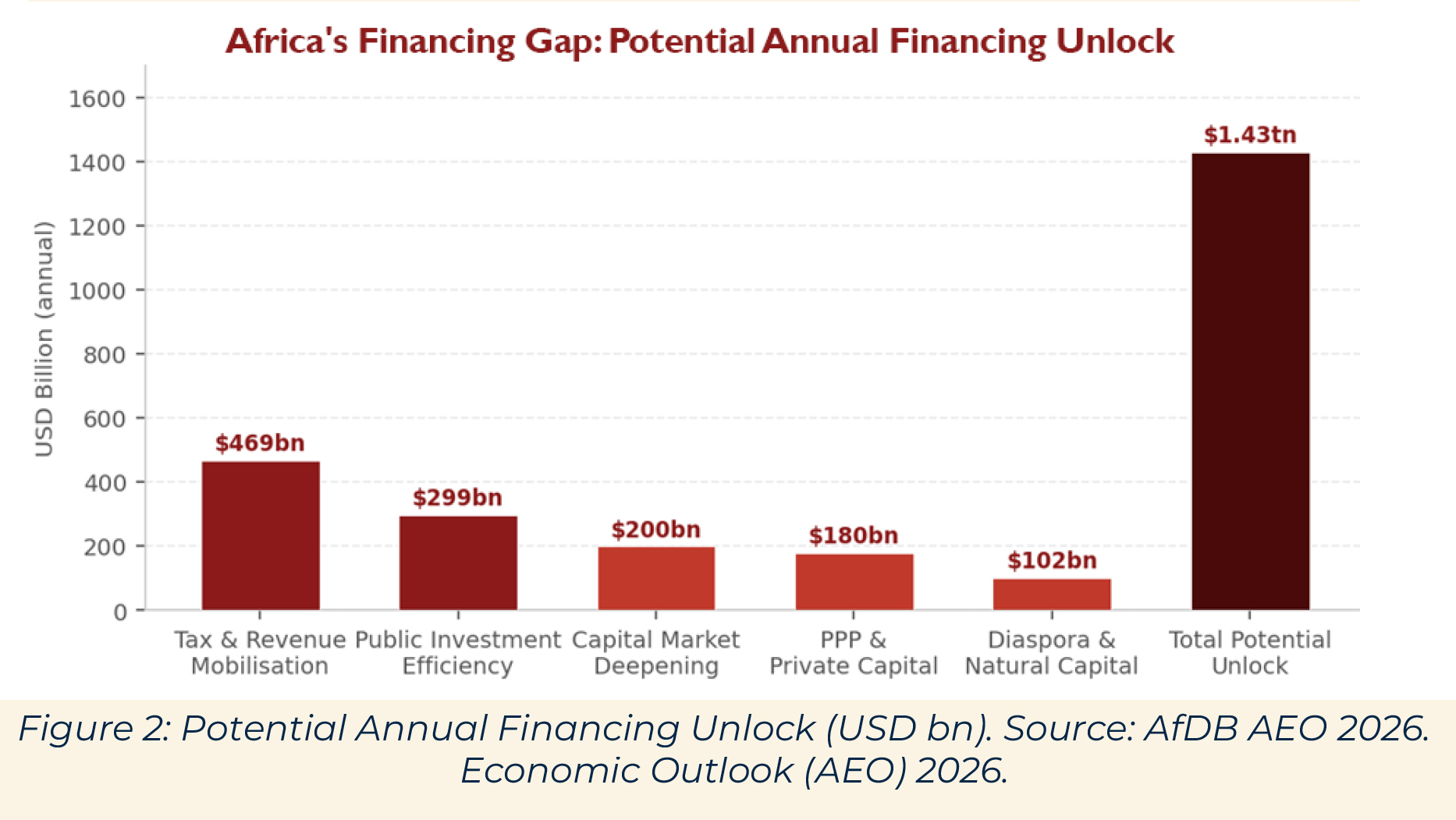

The scale of opportunity is enormous. The Report estimates up to US$1.43 trillion in

annual financing could be unlocked through stronger domestic revenue

mobilisation, more efficient public investment, reduced illicit financial flows,

deeper capital markets, expanded public-private partnerships, diaspora financing

and better utilisation of natural capital.

Two figures stand out: approximately US$469 billion in additional annual revenues

from improved tax and non-tax mobilisation, and a further US$299 billion in

potential savings through more efficient public investment. Each has a direct legal

dimension.

Strengthening domestic revenue mobilisation requires legislative reform, modern

tax administration frameworks and international cooperation mechanisms

capable of addressing base erosion and profit shifting. Improving public

investment efficiency requires robust procurement frameworks, transparent

project selection processes and effective public financial management systems.

Deepening capital markets requires sophisticated securities regulation, fund

governance frameworks, investor protection regimes and insolvency systems

capable of supporting increasingly complex financing structures.

The Report also highlights a powerful multiplier: each additional dollar of public

expenditure mobilises approximately US$1.40 in private capital. But that effect is

not automatic. It depends on the quality of legal and contractual frameworks

governing private participation, concession arrangements, government support

mechanisms, off-take structures, dispute resolution frameworks and regulatory

certainty.

In practice, bankability is determined not by project economics alone, but by the

legal architecture that underpins revenue certainty, allocates risk and provides

confidence in contractual enforcement.

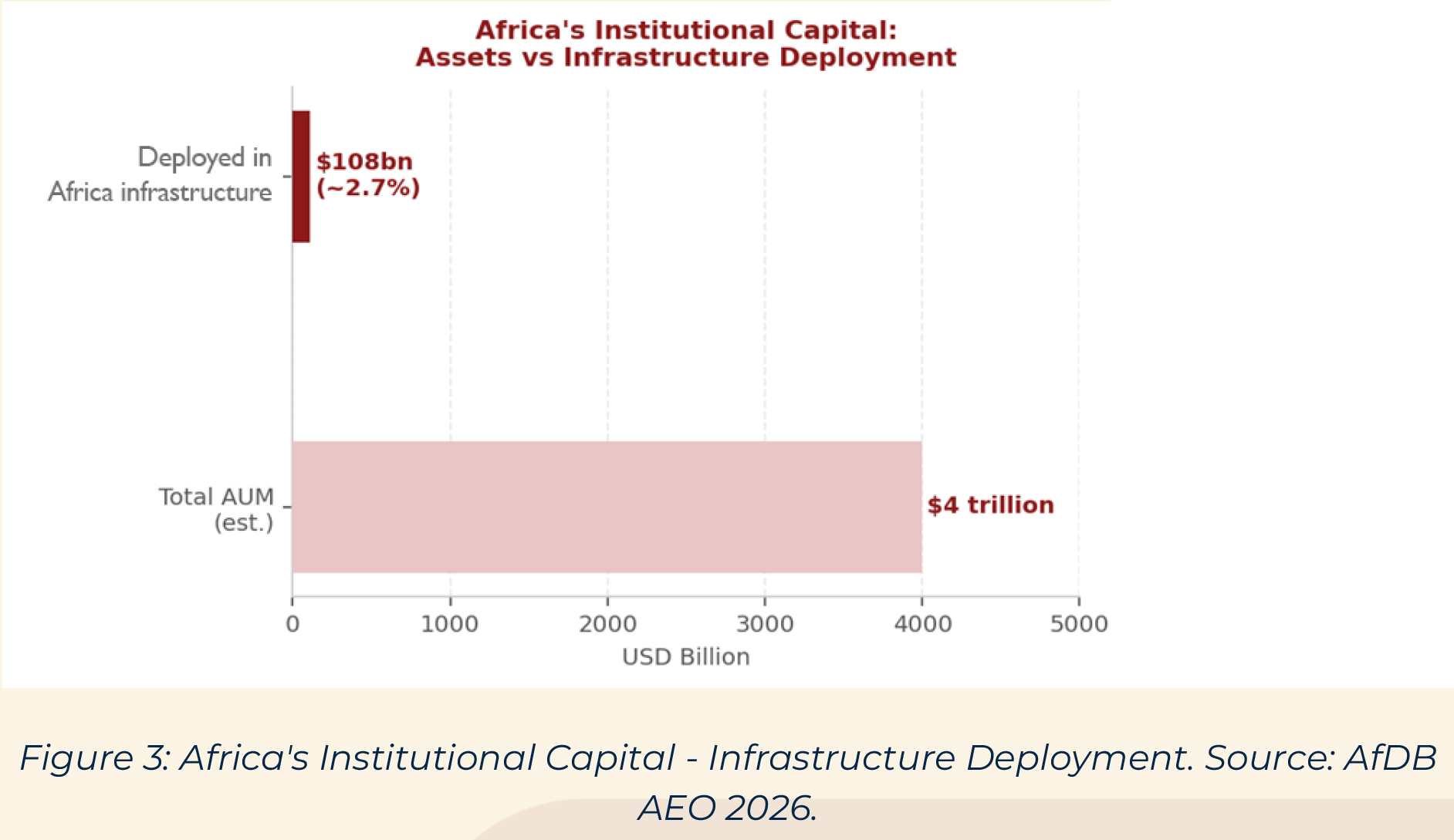

Here is the Report's most striking structural observation: Africa is not short of

capital. The continent's pension funds, insurance companies and sovereign wealth

funds collectively manage approximately US$4 trillion, yet less than 2.7 percent

goes to infrastructure and productive sectors within Africa. The problem is not

availability, it is deployment.

This mirrors the Africa Finance Corporation's State of Africa's Infrastructure Report

2026, which similarly identified deployment, not availability, as Africa's principal

development constraint. Both reports reach the same conclusion: the institutions

and mechanisms channelling long-term savings into bankable investments must

be strengthened.

Scaling deployment demands institutions with the mandate, balance sheet

capacity and technical expertise to bridge fragmented pools of savings and long-

term investment opportunities, and the legal frameworks that enable them to

function.

The Report places significant emphasis on the New African Financial Architecture

for Development (NAFAD), which seeks to leverage Africa's institutional asset base

through pan-African financial institutions, integrated capital markets and

innovative financing structures, including climate finance and Islamic finance

instruments.

Building NAFAD is, at its core, a legal project, requiring enabling legislation,

governance frameworks, regulatory coordination and sophisticated multi-

jurisdictional structuring.

The launch of the African Credit Rating Agency represents another important

institutional development. Addressing perceived biases in sovereign risk

assessments has implications that extend beyond market perception. More

accurate risk pricing has the potential to reduce borrowing costs, expand access to

institutional capital and support the development of deeper local currency debt

markets capable of financing long-term infrastructure without exposing borrowers

to significant currency mismatch risk.

Africa's stock market capitalisation hit US$1.2 trillion in 2024, nearly sixfold growth

in two decades. Yet activity remains concentrated in just four markets: South Africa,

Egypt, Nigeria and Morocco.

Capital market integration is both a financial imperative and a legal undertaking.

Fragmented systems impede capital mobility and drag on resource allocation

efficiency. The African Continental Free Trade Area and regional economic

communities have made progress, but significant barriers remain.

Greater integration has the potential to expand investor pools, reduce financing

costs and improve access to long-term capital. Achieving those outcomes will

require harmonised securities regulation, enhanced regulatory cooperation,

frameworks for investment products, standardised disclosure requirements and

legal frameworks capable of supporting cross-border investment activity.

The Report also highlights the African Financing Stability Mechanism, intended to

strengthen financial stability, ease liquidity pressures and support sovereign debt

management. Its credibility will depend on its legal foundations: institutional

mandate, governance structure, voting arrangements, creditor status framework

and intergovernmental agreements. These are not technical details, They are

fundamental determinants of the mechanism's effectiveness.

The Report's central message is clear: Africa's development challenge has shifted

from raising capital to deploying it, through institutions, markets and legal

frameworks capable of supporting long-term investment.

The NAFAD framework, the African Credit Rating Agency, the African Financing

Stability Mechanism and the public-private partnership agenda highlighted

throughout the Report are, at their core, exercises in legal and institutional design.

Their success will depend on the quality of the legislation, governance structures,

transaction frameworks and regulatory systems that underpin them.

For governments, this means strengthening institutions, enhancing regulatory

certainty and creating environments that attract long-term investment. For

investors, it presents significant opportunities across infrastructure, energy,

financial services, industrial development and capital markets. For legal advisers, it

reinforces the growing importance of sophisticated structuring, regulatory design

and transaction execution in shaping Africa's next phase of development.

At Parsons, we view the Report as more than an economic assessment; it is a

roadmap for the legal and institutional reforms that will underpin Africa’s future

growth. Our work across development finance, infrastructure, project finance,

capital markets, energy and cross-border investment places us at the centre of

many of the themes it identifies.

As Africa turns inward to finance its development, the strength of its legal

architecture becomes a decisive factor in economic success. At Parsons, we advise

across this full spectrum, working with investors, project developers, development

finance institutions, pension fund managers and governments on the legal

frameworks that enable the transformation described in the Report. Our practice

spans development finance and capital markets, energy and infrastructure,

regulatory compliance and cross-border investment structuring, with offices in

Lagos, London and the UAE, and a focus on the markets where this work is most

consequential.

For further information on how Parsons can support your engagement with Africa's development finance, capital markets and infrastructure landscape, contact us at info@parsons-legal.com or visit www.parsons-legal.com.